Lecture 2

2023-03-23

MIT OCW 14.01SC L2 - Application of Supply and Demand

MIT OCW 14.01SC - Lec 2 (Youtube)

-

Supply and Demand

- Demand

Q_d = D(P)

dQ_d / dP < 0- Demand curve may shift due to changes in variables other than price.

- Market demand is equal to sum of consumer demand.

Q_m = \sum Q_i

- Supply

Q_s = S(P)

dQ_s / dP > 0- Also influenced by other variables, like input costs, technology.

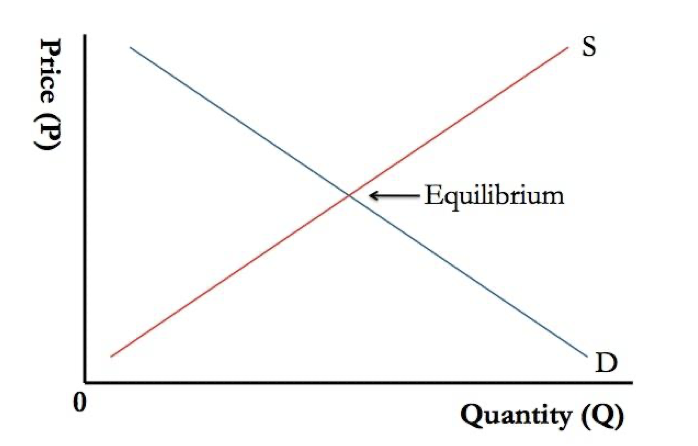

- Market Equlibrium

Q_d (P*) = Q_s (P*)P*is optimal price.

- Demand

-

Equilibrium shocks

- What happens when you change the equilibrium (through supply or demand shock)?

- Understand every concept on three levels: intuitive, graphical, mathematical.

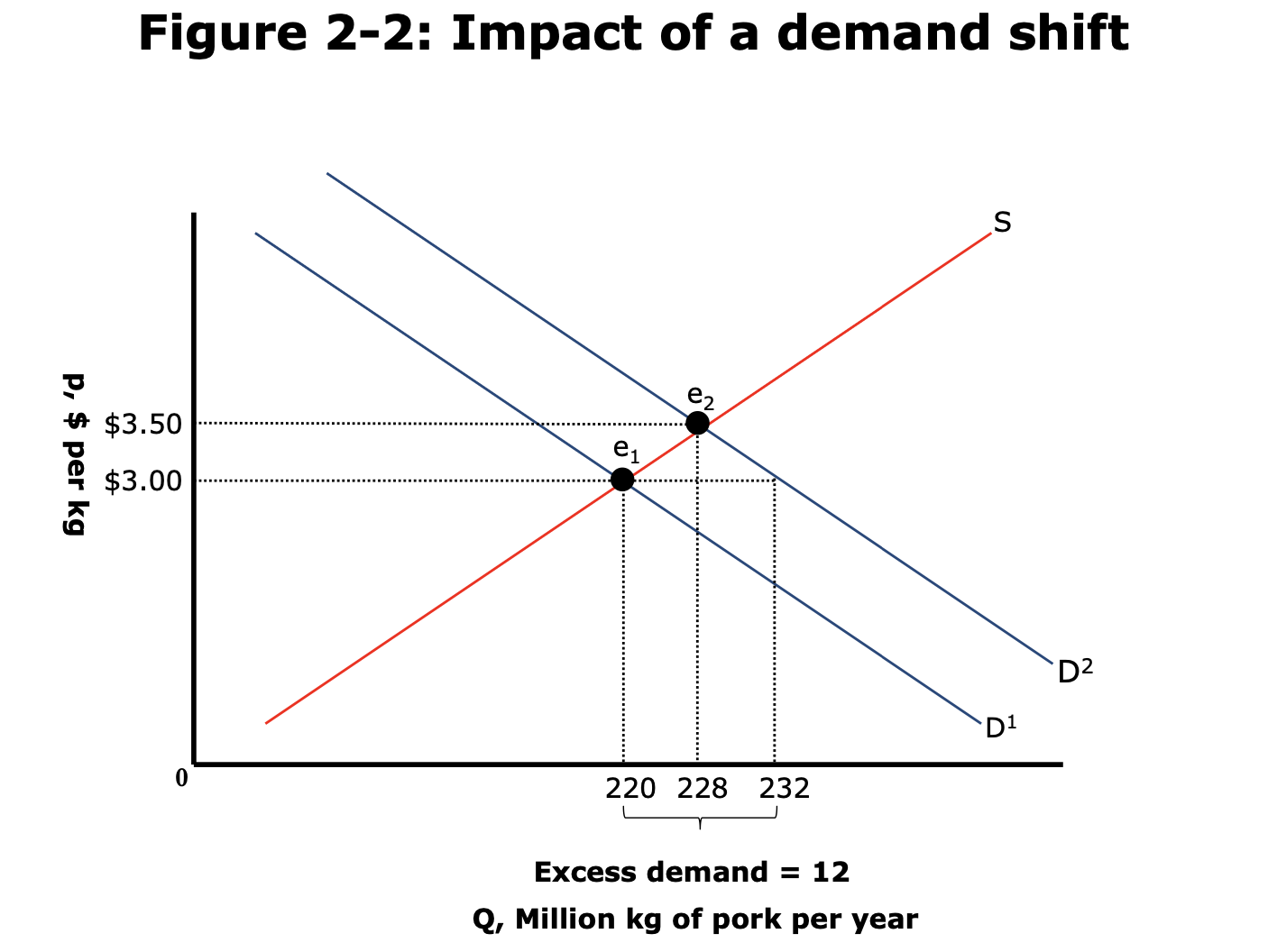

- Example 1. Price of substitute product increases, demand for good also increases. Demand curve shifts up (outward). There is new eqm.

- Initially: Excess demand.

- Slide up the supply curve to higher price at new eqm.

- General eqm: Markets may affect prices in other markets. Feedback effect where it affects the original price. (not in scope within this course).

- Where does supply curve come from? Producer theory - discussed later. (from firms trying to maximise their profits).

- Example 2. Price of producing good increases. Supply curve shifts upward (inward).

- Less ability to produce at the same price. Reduced supply.

- New eqm at higher price.

- In both situations (increased demand and decreased supply), the same thing happened! The price went up.

- From looking at the price alone it is not possible to tell which of these happened.

- However the volume was affected differently, in one the qty went up, in other qty went down.

-

Government Intervention

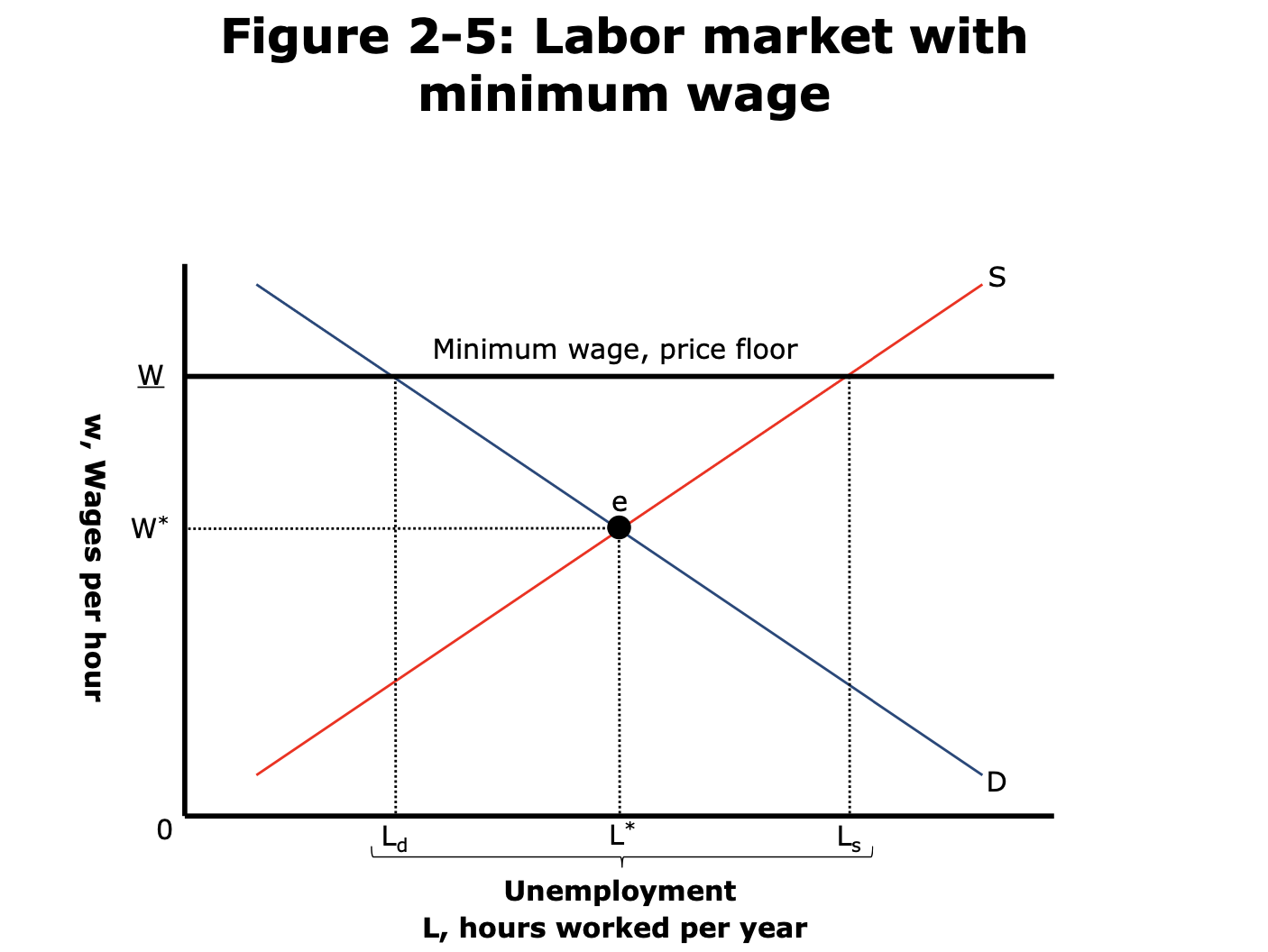

- Example: Minimum wage

- Consider market for Labour

- Labour is an input to the production process

- Firms demand labour, People supply labour. (flipped wrt. previous example of goods)

- At wage

W_(aboveW*), workers are delighted to workL_shours, but firms need onlyL_dhours.- Excess supply.

- Under perfectly competitive market conditions -> excess supply would cause demand to increase and wages would fall.

- But you can't do that now because of the govt.

- We call the excess supply 'unemployment'.

- Disequilibrium -> market condition still exists at

(L_d, W_)-> determined by constraint.

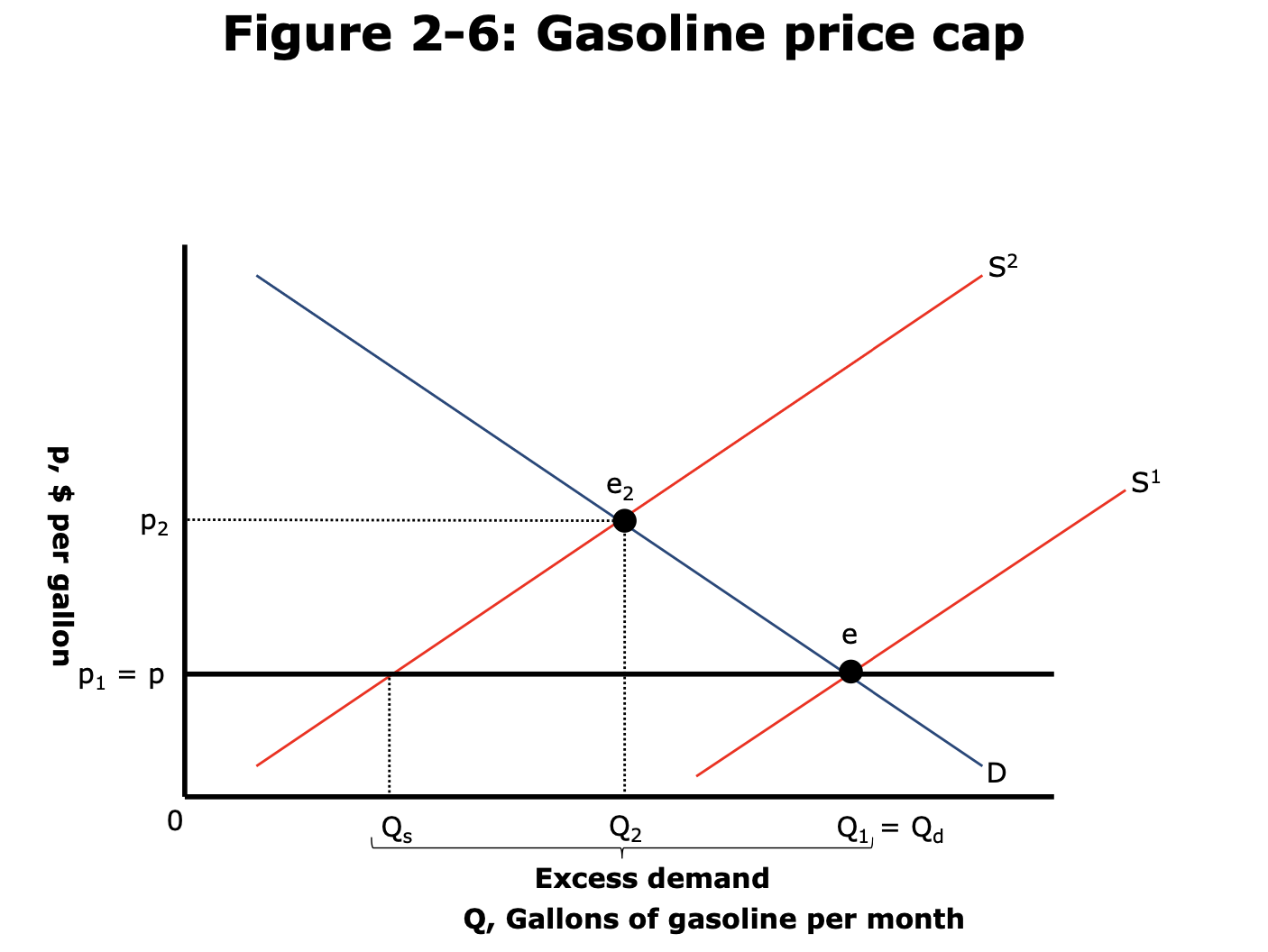

- Example 2: Gas price ceiling.

- Price capped at

p1, eqm was atp2. - Excess demand now. Eqm shifts to new point with lower qty being supplied at lower price.

- Price capped at

- Markets are robust and will do whatever they can to restore equilibrium!

- Welfare economics of this restriction?

- Costs:

- Efficiency loss: A trade that could have made both parties better off is not made.

- Allocation inefficiency: Lines at the gas station. Gas shortage. (Hoarding?)

- Benefit:

- Equity: Fairness

- Direct effects (what voters see) and indirect effects (what economists see).

- Equity-Efficiency tradeoffs.

- Secondary markets can arise to evade government regulation.

- Costs: